FXOpen

It’s been a while since I shared my ideas on market analysis with you. I see that reader interest in the topic increases. Especially for those who are trying to understand the true causes behind the price movements in a particular market.

So today, I want to move from theory to practice and based on data obtained in the COT report on 18th November 2016 to make a detailed analysis of one of the markets. My goal is to show you how I do it, so that you would be able to use this data in your trading.

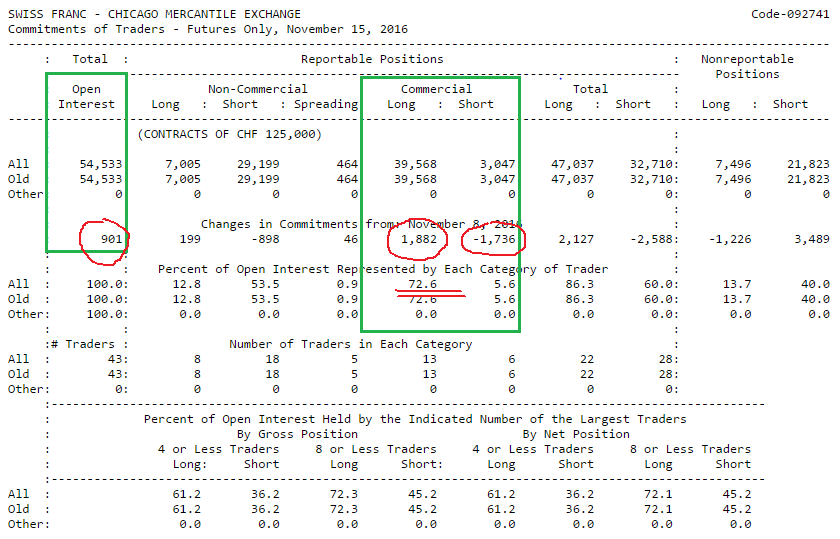

Let`s begin! Today we`ll look at the futures market Swiss franc. Below you can see the COT report for this instrument of November 15, which we received on Nov 18. Just a quick reminder: CFTC publishes this report every Friday, where the data originates from last Tuesday, i.e. we obtain this data with a three-day delay.

This is a very important factor to be considered, but we should not doubt that it is still relevant. I`ll show it today.

Analyzing the COT Report

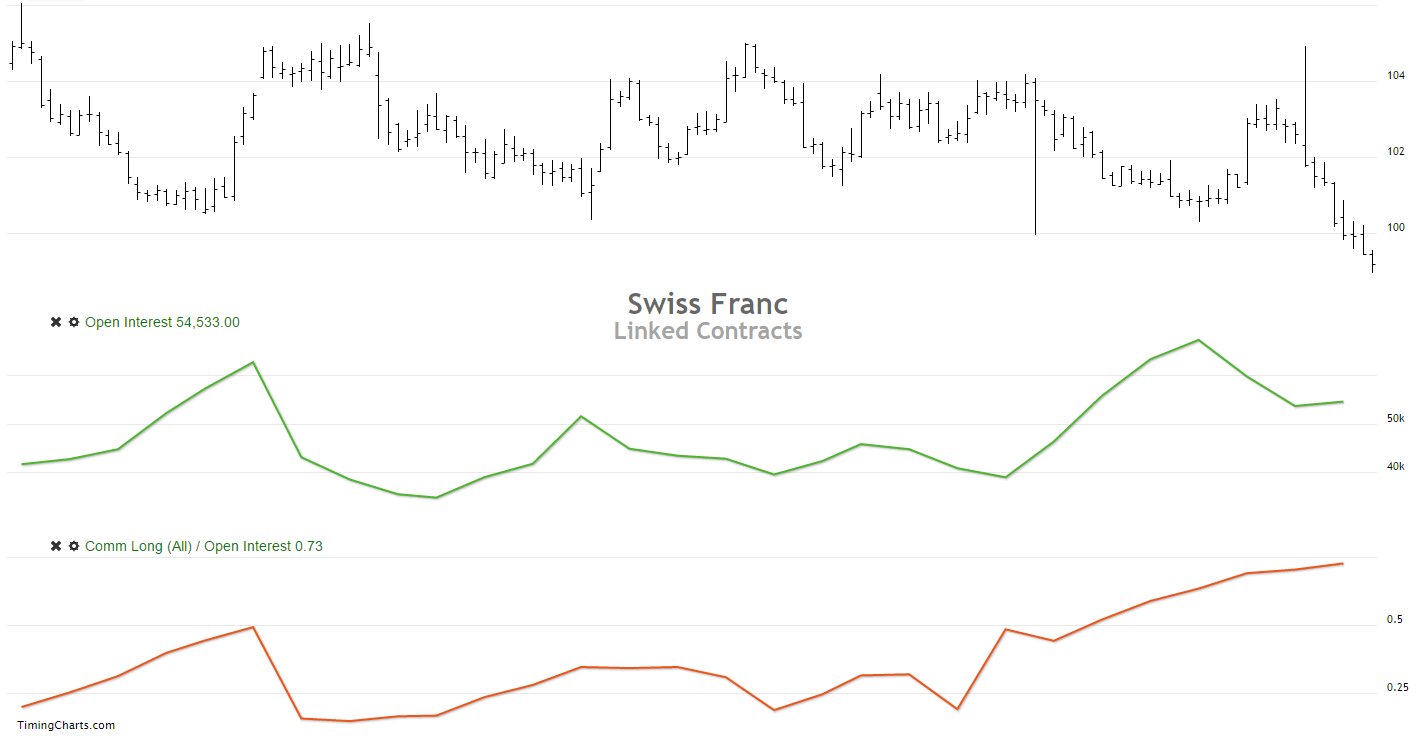

In this report, I`m mainly interested in changes of two columns marked green. The first one is the total number of open positions (Open Interest). The second one shows us the changes in the structure of commercial participants’ (Commercial) open positions.

Here we can see that during the reporting week of November 8th – 15th, the total number of open positions changed insignificantly. The amount increased just to 901 contract. In addition, during this period the operators have increased their long positions (1882 contract), cut their shorts (-1736 contract) and had a net long position of 36521 contract (39568 – 3047 = 36521). It is also worth noting, that the share of commercial participants’ long positions to the total volume of open positions is 72.6% (39568 / 54533 * 100 = 72.6). Now, let`s open the chart and see, how the price changed during this period.

What Do We See on the Chart?

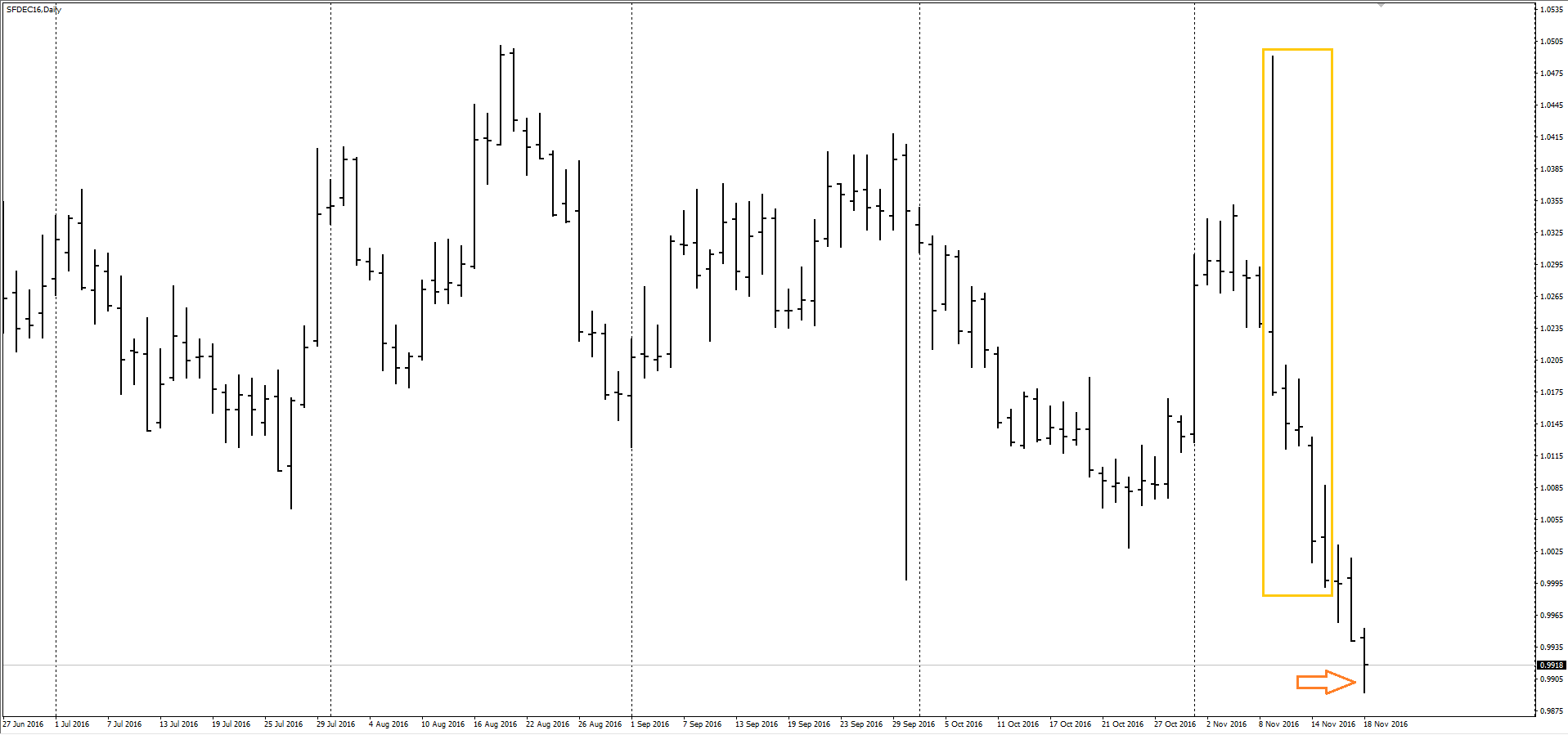

Here I have outlined five trading sessions of the reporting week and noted the day, when this data was published (when we received these data at our disposal).

The price was falling during the five days and finally on November 15, has updated the lows of June 2016. For the next three days after that, while the report has not been published yet, the price continued its decline. Significant changes during this three-day period has not occurred, except that the price has not dropped even lower. On this basis, I conclude that the data presented in the report remains valid.

What Relative Indicators I Use

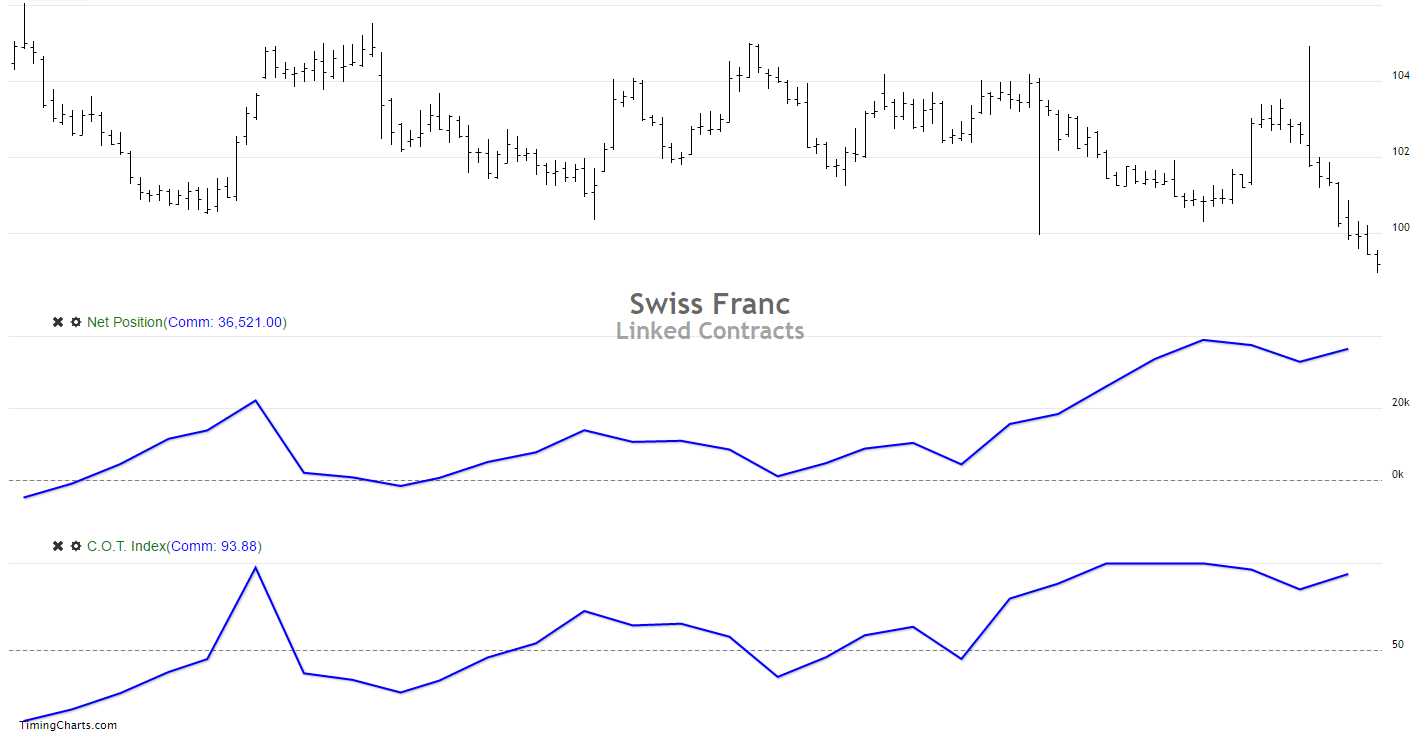

It`s time to compare the data obtained in the report with historical values to assess the strength of their influence on the market. I`m using Timing Charts for it. Here we have the opportunity to compare not only absolute values presented in the COT report, but the relative values as well. I am personally convinced, that it is much easier to work with relative figures than with absolute.

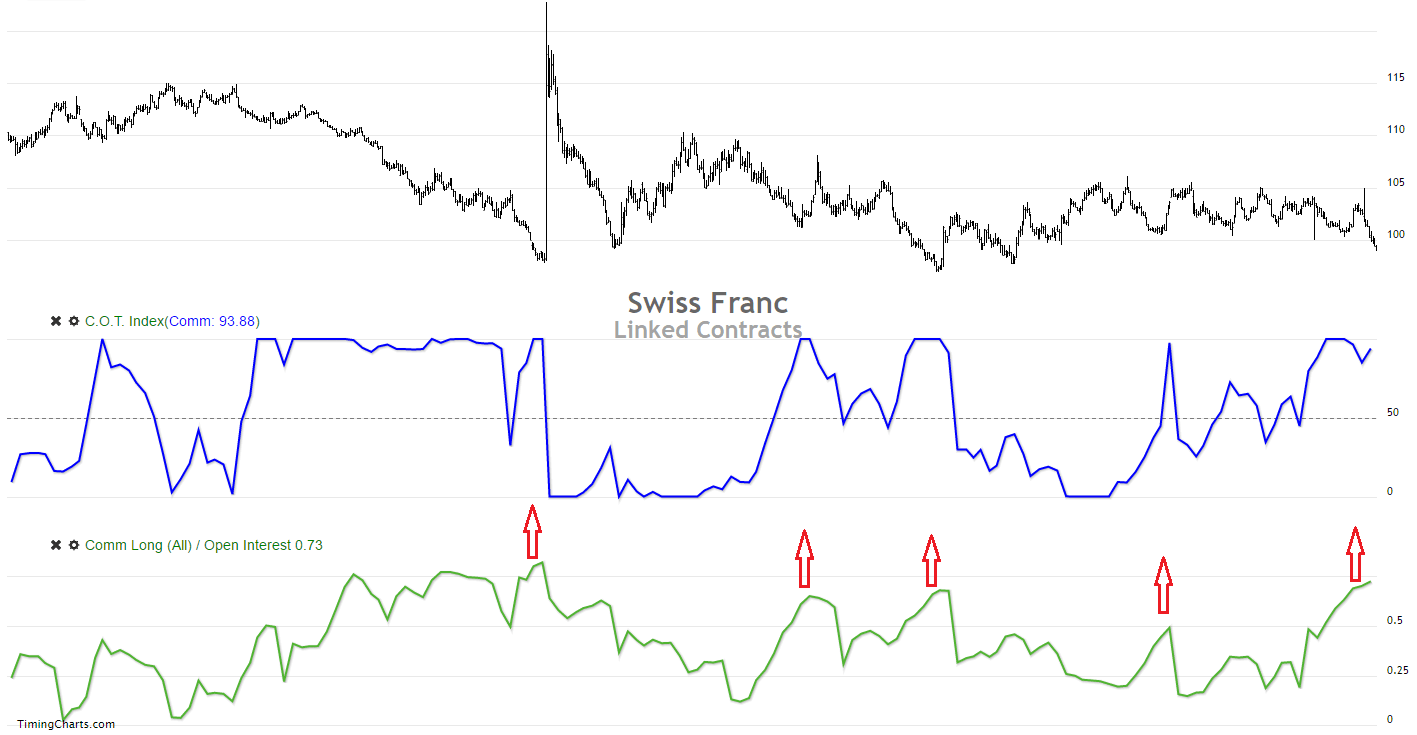

COT Index

The first relative measure I use is the COT Index. You can see this indicator at the bottom of the image, just below the changes of net open positions of operators. Despite the fact that visually the two curves are identical, in trade when you need to determine the reference levels, it is easier to operate with relative values, because these values will always be in the same range. This index compares a current net open position with the high and low for the last 26 weeks (six months). You can change the number of weeks involved in the index calculation at your discretion, but I use 26 weeks.

C.O.T. Index = (Current Net Position – Minimum Net Position [Weeks]) / (Maximum Net Position [Weeks] – Minimum Net Position [Weeks])

Let`s imagine that this indicator shows 100%. This would mean that currently we have the maximum net long position of operators for the last 26 weeks. Otherwise, if this index will show 0%, this will tell us that operators now have the maximum net shorts over the same period.

Open Interest Percent

Another relative indicator that I use you can find in the report (Image 1). This is the percentage of commercial participants’ open long or short positions in the total open interest. If the COT index is above 80%, as in our example, I use the following formula:

Open Interest Percent = Commercial Long / Open Interest

If the COT index is below 20%:

Open Interest Percent = Commercial Short / Open Interest

In our case, the COT index is 93.88%. On the chart below, in addition to the absolute value of Open Interest changes I reflected changes in long position of operators regarding the same value (Comm Long / Open Interest).

We`ve got a coefficient of 0.73 after rounding or 73 percent. This means that in the total open long positions 54533 contract, 73 % or 39568 contracts constitute a long position of operators and only the remaining 27 % distributed among other groups. At the same time, if we look at the total volume of short positions the same 54533 of the contract, the operators keep only 3047 contracts or 5.6 % of the total.

Conclusion

Currently, the operators hold almost the maximum net long position of 93.88% over the last 26 weeks. In addition, the share of operators’ long positions to the total volume of open interest is 73% and continues to grow. Increasing this share, it increases the probability the price will reverse.

If we look at the changes in history of this indicator, we can see that the price changed its direction when the value was smaller.

For this market, I believe the conditions will be met if the COT Index is above 80% or below 20%, while Open Interest Percent is greater than 60% or 50%, respectively. For other markets, generally, the control values of the first indicator remain the same 80% and 20%, while the second one may vary from market to market. It is easy to identify them, just by looking at the history and determining for which Open Interest Percent values there was a trend change.

This does not mean that after the value reaches these targets, I will immediately open a trade. As I said before, the conditions mentioned above are only one of three points to be checked when opening a trade. Therefore, only after meeting these criteria I`m starting to use the technical analysis tools solely in order to enter the market.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Latest articles

AUD/USD Rises Sharply on Inflation News

The Consumer Price Index for Australia was released this morning. According to ForexFactory:

→ CPI in quarterly terms: actual = 1.0%, expected = 0.8%, previous value = 0.6%;

→ CPI in annual terms: actual = 3.5%, expected = 3.4%, previous value = 3.

TSLA Share Price Up About 13% Despite Disappointing Report

Yesterday, TSLA trading closed at USD 144.68 per share, after which Tesla reported its results for the 1st quarter:

→ earnings per share: actual = USD 0.45, forecast = USD 0.49;

→ gross income: actual = USD 21.45 billion, forecast = USD

Market Analysis: Gold Price Corrects Gains While Oil Price Regains Strength

Gold price rallied above $2,400 before correcting lower. Crude oil price is rising and it could climb further higher toward the $85.50 resistance.

Important Takeaways for Gold and Oil Prices Analysis Today

· Gold price rallied significantly above $2,